Resilience versus robustness in global value chains: Some policy implications

Reprinted with permission from VoxEU

By Sébastien Miroudot, Senior Economist at the OECD Directorate for Science, Technology and Innovation

Some governments assert that global value chains create economic vulnerabilities in times of a pandemic. This column, taken from a recent Vox eBook, examines recent experiences and the risk-management literature. It concludes that it is a mistake to equate self-sufficiency with robustness – putting all the eggs in one basket is still not a good idea. It is also a mistake to focus on production location when the imperative is to radically scale up production of vital medical supplies. Importantly, international supply chains will be needed to produce the billions of doses of COVID-19 vaccine we will soon need to manufacture and distribute.

With the COVID-19 crisis, a new debate has emerged with respect to global value chains (GVCs), examining whether excessive globalisation of production has not created new economic vulnerabilities. For example, Beata Javorcik recently wrote in the Financial Times that “businesses will be forced to rethink their global value chains” and that “while just-in-time manufacturing may be the optimal way of producing a highly complex item such as a car, the disadvantages of a system that requires all of its elements to work like clockwork have now been exposed”.1 Even the World Economic Forum has recommended to “aggressively evaluate near-shore options to shorten supply chains and increase proximity to customers” as a response to COVID-19.2

This column first appeared in the Vox eBook COVID-19 and Trade Policy: Why Turning Inward Won’t Work, available to download here.

While some lessons will have to be drawn, and both firms and consumers are likely to make different choices after the crisis, it may be premature to call for the end of GVCs or to conclude that shorter supply chains would be less vulnerable. This chapter reviews the relevant management and business literature and highlights evidence to show that the relationship between GVCs and resilience or robustness in the supply of inputs is more complicated than it looks. Even in the midst of the COVID-19 crisis, we see how efficient GVCs are in answering the most urgent needs of countries. Policies in the future should support business efforts to build more robust and resilient supply chains and not add to health and other dangers a policy risk built on misconceptions about GVCs.

The vulnerability of supply chains during COVID-19

What are we exactly talking about when speaking of risk? On the supply side, firms face risks such as plant fires, natural disasters, financial risks, political instability, cyber-attacks, quality issues with suppliers and delivery failures. On the demand side, those risks include reputation of products, new competitors, policies restricting market access, macroeconomic crisis, and exchange rate volatility.

COVID-19 is first and foremost a global health crisis and has impacted the production of firms in GVCs in several ways.

- Production was stopped or disrupted because firms were directly affected by the presence of the virus at production sites.

Whether it was a decision coming from the government or from the firm itself, either there was a need to stop producing or to maintain production with new rules guaranteeing the safety of employees (with an impact on production such as delays or reduced output). This type of risk is related to the production site and applies to all firms in the same location. However, firms that source inputs from different locations confront an additional risk - even if the virus does not affect the production site, they nevertheless need inputs originating from a potentially affected area.

This is a supply chain risk. For example, such risk materialised in the fourth week of January 2020 when China decided to lock down the city of Wuhan and start taking measures to prevent the spread of the virus to the rest of the country. Manufacturing companies in the rest of the world (unaware at this stage of the tsunami that was about to hit them) were quickly hit. Car manufacturer Hyundai halted all production in Korea on 7 February 2020 due to a shortage of components coming out of China. This type of contagion flowing through GVCs has also been observed with some natural disasters, such as the earthquake and tsunami in Japan in 2011, or the floods in Thailand that same year.

Within a matter of only a few weeks during February 2020, the virus spread rapidly to other regions, first to Europe and then to North America. Such was the speed of its spread that supply chains were hardly disrupted. It wasnít until 19 March that Ford stopped its production of cars in both North America and Europe. And there only four days separated Volkswagen closing its factories in Europe (17 March) and in the US (21 March).3 And whether domestic or not, suppliers of parts and components also closed their plants because they were affected by similar measures - not because their inputs could not be delivered; the contagion became more of a concussion (Baldwin 2020).

Transportation is also a source of risk. For those companies still producing during the lockdowns (and possibly for all companies once lockdowns are lifted and the virus is still present), the vulnerability of international supply chains will depend on whether international transportation networks are still operating and without significant increases in trade costs.

- While limiting trade in goods was not part of the health response (with the important exception of export bans and restrictions to trade for some key medical supplies and medicines), measures taken by governments limiting the movement of people or reinforcing border controls have, to some extent, led to the disruption in international trade.

Trade in services is directly impacted when it relies on the movement of consumers (e.g. tourism) or the movement of producers (e.g. many business services but also transport services).

Goods are moved across countries through services, and trade in goods is indirectly impacted by the measures affecting (those) services. This is especially the case for air freight, which has been relying on cargo holds in passenger planes and is favoured during the crisis to reduce the delivery time of key inputs and supplies. Quarantine measures for air or sea crews and additional sanitary controls related to COVID-19 (or measures to protect the people in charge of controls) are also delaying trade.

While domestic transport networks and logistics are also disrupted, there is an additional vulnerability for international freight and a risk specific to international production networks. However, it is difficult to assess the level of disruption to international trade currently. Most logistics firms report no strong impact on their operational capabilities with the exception of some air routes or specific destinations that may be more impacted by the virus.4 Volatility in freight rates has risen, but with falling demand, international trade costs are more likely to decrease than to increase.

All the above risks are on the supply side and were mainly the focus of most debates on the level of vulnerability in international supply chains. However, on the demand side, an even greater risk may be on the horizon – culminating in a profound worldwide economic crisis triggered by lockdowns and restrictions to movement of people (which also restrict consumers ability to consume).

Contagion through GVCs will again become a concern if regions lift these restrictions sequentially and if the economic impact, although profound, is more or less severe across different areas. The mechanisms, which were observed during the 2008-2009 Global Financial Crisis via contagion through declining demand and amplification effects (Bems et al. 2009) will resurface. However, the COVID-19 crisis is of a different nature, with the recession likely to stem from services and domestic activities rather be associated than trade finance issues, as in 2008-2009. The macroeconomic implications are also different (Guerrieri et al. 2020).

No current evidence that complex supply chains are more impacted by COVID-19

Numerous statements have been made about complex value chains being more impacted during the COVID-19 crisis, possibly due to additional risks and costs related to international trade.5 However, the available evidence – while limited at this stage ñ does not support such a view. The most impacted industries are those relying on the movement of people, such as hotels and restaurants, or passenger transport. And for countries under a lockdown, the bulk of the impact is through the fall in domestic demand and not international tourists.

The most impacted industries are those relying on the movement of people, such as hotels and restaurants, or passenger transport. And for countries under a lockdown, the bulk of the impact is through the fall in domestic demand and not international tourists.

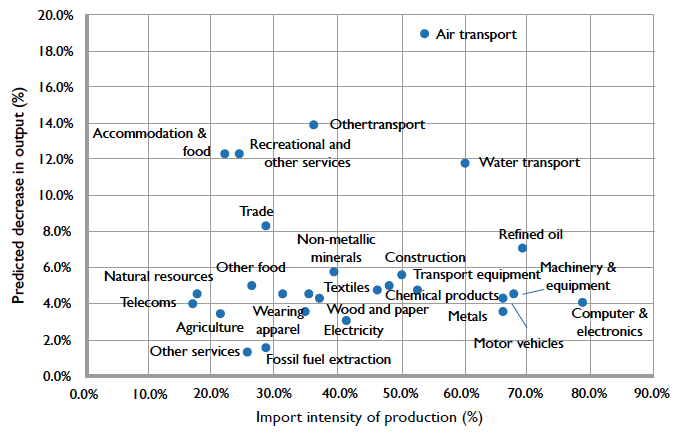

Figure 1 is based on World Bank estimates of the economic impact of COVID-19 made on Thailand (Maliszewska et al. 2020). This country is an interesting example due to its integration in manufacturing GVCs as well as tourism activities. For each sector, the decrease in output is the consequence of some level of under-utilisation of capital and labour, increase in international trade costs, and a decrease in any activities that involve proximity among people. As the pandemic is still ongoing, these figures are model predictions only and not observed data. They are plotted against the import intensity of production, which can be interpreted as an index of the level of fragmentation of production (Timmer et al. 2016). Data come from the OECD Trade in Value-Added (TiVA) database.

Figure 1 Import intensity of production and predicted decrease in output in Thailand, by sector (%)

Source: Maliszewska et al. (2020) and author’s calculations with the OECD TiVA database.

There is no correlation between the level of fragmentation of production and the severity of the economic impact of COVID-19, not only because of services activities but also among manufacturing industries. For example, textiles and apparel is an industry that relies less on imports of inputs in Thailand when compared to the computer and electronics industry. But both have a similar predicted decrease in output. The computer and electronics industry has the highest level of fragmentation of production. Nevertheless, this industry is likely to be less impacted than retail and wholesale trade or accommodation and food services.

Resilience in GVCs is not the same as robustness

The risk management literature makes an important distinction between resilience and robustness in supply chains.

- Resilience can be defined as the ability to return to normal operations over an acceptable period of time, post-disruption.

- Robustness is the ability to maintain operations during a crisis (Brandon-Jones et al. 2014).

- Building robustness requires different strategies, when compared to building resilience, and when it comes to the distribution of key medical supplies (such as face masks, ventilators, medicines), it is robustness that matters, not resilience.

For example, the redundancy in suppliers or alternative locations of production is a strategy for robustness. Firms that have diversified suppliers and a production network across different countries can adjust their production when a disaster occurs in one place. After the earthquake in Japan in 2011, the experience led to manufacturers in the motor vehicles industry diversifying their suppliers (Matous and Todo 2017).

Fully localised production is not recommended for robustness as the disaster can happen within a domestic economy. This can be illustrated with the example of Samsung Electronics which generally produces its latest generation of smartphones within Korea, but older generations are manufactured abroad. The main plant is near the city of Daegu, the epicentre of COVID-19 in Korea at the end of February 2020. When the disease was discovered among its workers, factory immediately halted all activities for several days. Samsung then decided to switch part of its smartphone production to Vietnam where it operates other factories.6

Nevertheless, the geography of production is not the main element of strategies of firms interested in withstanding disruptions. Management literature insists more on information sharing as well as the visibility of supply chains. To anticipate disruptions, it is important to know exactly the level of inventories, as well as output all along the value chain.

- Large multinational enterprises (MNEs) develop ‘control towers’ and information systems that give accurate real-time information on production networks, and these tools allow for an efficient management of risks, independent of production and length of supply chains.

The complexity of the network is an important variable, but the approach of firms is not to simplify the network (since this network exists to improve performance) but rather to invest in tools for dealing with this complexity and to introduce some reactivity and flexibility in operations. Since important costs are associated with robustness, such as investing in tools that allow the monitoring of risks, some companies are more interested in resilience in their supply chains. They accept the risk that production can be stopped, but nevertheless invest in reducing the time needed for recovery.

Resilience can be built in different ways:

- Through products (with buffer stocks and standardised inputs easier to be replaced);

- Through the design of the value chain (identifying places and suppliers less subject to risk); and

- Through resilience monitoring (assessing the time to recover for each type of supplier).7

Some strategies are common to resilience and robustness, but the difference is that resilient firms tend to reduce their risks but will not invest significantly to anticipate and avoid all types of disruptions. Such firms prefer to go through the disruptions and minimise their impact.

This is why single sourcing and a long-term relationship with a single supplier is a strategy often observed for improving supply-chain resilience. This strategy is not optimal in terms of robustness when this supplier is affected by a risk. However, instead of switching to other suppliers and possibly incurring sunk costs, it can lead to further investment from the supplier for facilitating recovery, as well as a shorter and less-costly disruption in the end.

There is empirical evidence that supplier diversification is associated with a slower recovery from supply disruptions, whereas the use of long-term relationships is associated with more rapid recovery (Jain et al. 2016).

Lessons from the tsunami in Japan and floods in Thailand in 2011: More offshoring

The experience with the 2011 tsunami in Japan and floods in Thailand is that ‘complex’ value chains are not always robust and they take the full hit of both the direct effect of the disaster and indirect contagion effects through their respective supply chains. But they are quite resilient. In Japan, most plants that were directly hit by the earthquake restarted all activity within three months (Inoue and Todo 2017). While ‘complex’ supply chains are a source of increased risks, they nevertheless provide a network of trading partners and economic gains that can facilitate recovery. Looking at firm-level data, Todo et al. (2015) find that firms with extensive networks of suppliers had a quicker recovery and they conclude that the positive effects of supply chains typically exceed the negative effects. Zhu et al. (2017) highlight that firms in the area affected by the earthquake responded by increasing offshoring activities.

The Chao Phraya river floods in Thailand the same year were a second major natural disaster, with a deep economic impact on the hard disk drive (HDD) industry for which Thailand was concentrating 43% of the production. The leading firm in the HDD industry, Western Digital, had its factories inundated while its rival, Seagate, had factories in the same place in Thailand but located on elevated grounds (Haraguchi and Lall 2015). Some of Toshiba’s factories were also inundated, but the company could divert production to the Philippines. However, it took only six months for Western Digital to retake the lead in the market and 2012 was actually a record high for the production of hard disk drives. While many observers were expecting more diversity in the location of production after the 2011 experience, it happens that Western Digital not only continued to produce in Thailand but also decided to close a factory in Malaysia in 2017 to concentrate even more its production in Thailand.8

In the midst of the COVID-19 outbreak, countries still rely on GVCs to address shortages in the supply of essential medical goods

COVID-19 is a global crisis very different from the localised natural disasters that took place with the earthquake in Japan or the floods in Thailand in 2011. It is too soon to talk about resilience as we are still in the middle of the crisis. But it seems that GVCs are rather robust during the pandemic and are even used to address the shortages observed in the supply of essential medical goods.

In Korea, a new industry has emerged that exports COVID-19 test kits to more than 100 countries. These tests allow rapid identification of infected people and play a key role in limiting the spread of the coronavirus. There are now about 25 Korean companies that have received the authorisation to export these kits (and soon 40 are expected).9 Seegene, one of the biggest of these companies (with 400 employees):

- Started to develop a test for detecting the coronavirus on 16 January 2020 using artificial intelligence and big data systems.

- On 5 February 2020, it was ready with an initial test that was approved for use in Korea on 23 February 2020.10

- One month later, the company was producing 1 million test kits per week and by the beginning of April 2020, production was increased to 3 million test kits per week, with 90% available for export.

Providing the latest generation of COVID-19 test kits to governments all around the world in a few weeks is a feat that would not have been possible without leveraging GVCs. It happened in Korea because it’s the G20 economy with the most integrated GVCs. The country was already producing in-vitro diagnostics (IVD) products before the crisis, but its main exports of medical goods were ultrasonic imaging devices and dental implants. Shifting an industry towards new products in such a short time requires international networks, skilled supply chain managers, reactivity, and agility. This type of experience simply does not come from local production and activities shielded from competition.11

Unlike face masks or ventilators where require heavy investments to be produced and where some inputs are not widely available, the production of test kits is accessible to most countries. The US or Europe have a large production capacity in In-Vitro Diagnostics (IVD). Indeed, lead firms there have developed COVID-19 tests and supplied their local markets. The main inputs are chemicals and reagents that are not difficult to manufacture (Korea is relying mostly on domestic supply). Since mass production of these tests needed to be organised in the last three months, one can wonder why the model of local production and re-shoring advocated by some was not followed by others, and why we see Korea exporting millions of test kits to Europe and the US.

Whether we consider face masks (where countries that can produce them such as France prefer to import billions from China rather than ramping up their national production) or test kits, it seems that GVCs are the preferred way to efficiently supply key COVID-19 goods during the crisis, despite their supposed vulnerability. This is a matter for further scrutiny post-crisis, and indicates that there are other factors at play ñ such as innovation, flexibility, reactivity, access to distribution networks, and so on ñ that accord an advantage to GVCs for the efficient supply of essential goods.

Concluding remarks

One motivation for introducing the concept of global value chains in policymaking was the need to understand business reality and how companies actually produce and trade goods and services. While it is acceptable to question GVCs in light of the COVID-19 crisis, business realities must guide policy deliberations.

GVCs have rendered important productivity gains and the main concern for post-COVID-19 scenarios based on the shortening of GVCs and re-shoring of activities is how to deal with a shock on productivity, while finding ways to recover from one of the biggest economic crises in history. The risk management literature has been looking at the resilience and robustness of supply chains for more than 20 years and does not propose that domestic production and short supply chains are the best way of addressing risks. However, it offers some guidance on different strategies, and in particular, highlights that some firms may look for robustness (e.g. medical supplies and medicines) while other may focus on resilience with different types of organisation of supply chains at the end.

The experience with previous crisis and disasters is that GVCs are rather resilient. Some sectors in the economy will be much more impacted by COVID-19 than the manufacturing industries operating in GVCs. For example, addressing the crisis in the air transport sector or tourism industry should be a higher priority than re-shoring the computer and electronics industry.

When it comes to distribution of essential goods such as medical supplies and medicines (possibly the reason for the current focus on domestic production and re-shoring), two pitfalls need to be avoided in future trade and investment policy discussions.

- The first mistake is to equate self-sufficiency or domestic production with robustness.

If the objective is to build more robust supply chains (without promoting a new mercantilist agenda), a combination of international trade and local supply is what works best. That is what Samsung found with its smart phones. And the process of deciding which sourcing strategies are the most adaptable should be driven by firms, since the answer will be different across sectors and even across companies. Policies that introduce new barriers to trade and investment to push firms towards domestic production or re-shoring would raise costs and lead to sourcing patterns driven by policy risks and not by the optimal organisation of production required for addressing other risks.

- The second mistake is to focus on the location of production; the overriding imperative during a crisis is to maintain and scale up production.

Some governments have been frustrated by the fact that in the middle of the COVID-19 crisis, their countries’ factories were not producing masks or ventilators. But countries with at least some production capacity were often faced with similar shortages in supply, and most of them ended up relying on trade rather than increasing their own production. When demand is suddenly multiplied by a factor of ten or more, governments and companies are compelled to switch to a different production model of production. In this light, it is unrealistic to think that a country can maintain and sustain an industry with the production capacity required at the time of the crisis. Anticipation, preparation and international co-operation can achieve better results, when compared to isolated and silo-based strategies.

In the near future, the mass production of a COVID-19 vaccine will require formidable international effort and cooperation. Scaling up production to allow a maximum of people to benefit from the vaccine in the shortest time possible can be achieved only through international production networks. Putting health considerations first requires having a fair assessment of what works and a solid reliance on production models that have delivered in the past. This is not the time for experimenting with untested new trade and industrial policies.

Author’s note: The author is writing in a personal capacity. The views expressed are those of the author and do not necessarily reflect those of the OECD Secretariat or the member countries of the OECD.

References

Baldwin, R (2020), “Supply Chain contagion waves: Thinking ahead on manufacturing ‘contagion and reinfection’ from the COVID concussion”, VoxEU.org, 1 April.

Bems, R, R C Johnson and K M Yi (2013), “The Great Trade Collapse”, Annual Review of Economics 5: 375-400.

Brandon-Jones, E, B Squire, C W Autry and K J Petersen (2014), “A contingent resource-based perspective of supply chain resilience and robustness”, Journal of Supply Chain Management 50(3): 55-73.

Guerrieri, V, G Lorenzoni, L Straub and I Werning (2020), “Macroeconomic implications of COVID-19: Can negative supply shocks cause demand shortages?”, working paper, 2 April.

Haraguchi, M and U Lall (2015), “Flood risks and impacts: A case study of Thailand’s floods in 2011 and research questions for supply chain decision making”, International Journal of Disaster Risk Reduction 14(3): 256-272.

Inoue, H and Y Todo (2017), “Mitigating the propagation of negative shocks due to supply chain disruptions”, VoxEU.org, 25 April.

Jain, N, K Girotra and N Netessine (2016), “Recovering from supply interruptions: The role of sourcing strategies”, INSEAD working paper No. 2016/58/TOM, August.

Maliszewska, M, A Mattoo and D Van der Mensbrugghe (2020), “The potential impact of COVID-19 on GDP and trade: A preliminary assessment”, Policy Research working paper No. WPS 9211, World Bank Group.

Matous, P and Y Todo (2017), “Analyzing the coevolution of interorganizational networks and organizational performance: Automakersí production networks in Japan”, Applied Network Science 2(5): 1-24.

Saenz and Revilla (2014), “Building resilient supply chains”, MIT Sloan Management Review, Summer.

Timmer, M, B Los, R Stehrer and G de Vries (2016), “An anatomy of the global trade slowdown based on the WIOD 2016 release”, GGDC Research Memorandum No. 162, University of Groningen.

Todo, Y, K Nakajima and P Matous (2015), “How do supply chain networks affect the resilience of firms to natural disasters? Evidence from the Great East Japan Earthquake”, Journal of Regional Science 55(2): 209-229.

Zhu, L, K Ito and E Tomiura (2016), “Global sourcing in the wake of disaster: Evidence from the Great East Japan Earthquake,” RIETI Discussion Paper Series, 16-E-089.

Endnotes

1 “Coronavirus will change the way the world does business for good”, Financial Times, 8 April 2020.

2 “Coronavirus is disrupting global value chains. Here's how companies can respond”, World Economic Forum, 27 February 2020.

3 “COVID-19 and plant closures: The automotive industry's response to the pandemic”, Road Show, 17 April 2020.

4 See, for example ,the daily information provided by BollorÈ Logistics (https://www.bollore-logistics.com/en/Pages/COVID-19.aspx) or Kuehne+Nagel (https://www.kn-portal.com/updates_on_coronavirus). These firms report many challenges but indicate that they are operational in most regions.

5 See, for example ,WTO trade forecasts released on 8 April 2020 at https://www.wto.org/english/news_e/pres20_e/pr855_e.htm.

6 “Samsung shifts some smartphone production to Vietnam due to coronavirus”, Financial Times, 6 March 2020.

7 See Saenz and Revilla (2014) for an example with Cisco Systems.

8 “Western Digital formats hard disk drive factory as demand spins down”, The Register, 17 July 2018.

9 “Korean-made COVID-19 testing kits demanded by over 100 countries”, Maeil Business News Korea, 9 April 2020.

10 “How this South Korean company created coronavirus test kits in three weeks”, CNN, 13 March 2020.

11 It would be interesting to further study how the impressive scale-up of production in China, in particular for face masks, was enabled by the experience of the country in GVCs as opposed to the leading role of the government and state-owned enterprises in the Chinese economy.