The long-run effects of climate change on the corporate sector: The case of Italy

Reprinted with permission from VoxEU

The question of whether firms are able to adapt to a changing climate is central to understanding the long-run economic effects of climate change. This column presents evidence from Italy showing that high temperatures affect firm demography by reducing the entry of newborn firms in the market and increasing business closures, while relocation to colder areas plays a minor role. Balance sheet data reveal a dichotomy between large firms, which successfully adapt improving their profitability, and smaller ones for which negative temperature spillovers become entrenched.

Climate change is one of the major structural challenges the global economy is currently facing (Blanchard and Tirole 2022), and economists are devoting a great effort to investigate its multifaceted implications (e.g. Weder di Mauro 2021). In particular, high temperatures substantially reduce economic activity and growth, especially in poor countries (see Kolstad and Moore 2020 for a recent review); advanced economies are not immune, with recent evidence documenting that unpredictable temperature shocks can also have aggregate consequences for the US economy (Natoli 2022). As climate-induced extreme events such as high temperatures are expected to become increasingly frequent without appropriate emission reduction policies, one key question in the current debate is how climate change could ultimately shape, at the aggregate level, a country’s productive sector.

This issue has been investigated from different angles. One of them explores the geographic dimension of global warming. Climatic phenomena may have heterogeneous impacts across space, possibly causing migration to low-risk areas, as investigated in a recent special issue of the Journal of Economic Geography (Peri and Robert-Nicoud 2021) and in Albert et al. (2021). Another aspect regards the direct implications of hot temperatures on firms (e.g. Addoum et al. 2020, Pankratz and Schiller 2021, Somanathan et al. 2021). During a heatwave, revenues can drop because workers in heat-exposed occupations can be less productive or more absent in hot days or, more generally, because high temperatures increase production costs. Over a longer time span, these effects may stimulate technological advancement for some firms and vanish, while they can accumulate and become persistent for others, increasing the likelihood of exiting the market.

While having potential effects on aggregate market structure, these possibly diverging paths have not received much attention in the literature. In a recent paper (Cascarano et al. 2022), we take up this issue by analysing the long-run impact of temperatures on the Italian corporate sector. We perform two analyses. First, using administrative data covering the entire Italian corporate sector, we explore how extremely hot temperatures affect local firm demography namely, entry, exit and relocation of firms across Italian local labour markets (i.e. areas that are internally homogeneous in terms of work commuting flows). Second, firm-level balance sheet data are employed to provide evidence on how temperatures can affect firm performance for those that survive on the market over the years.

Entry and exit from local labour markets

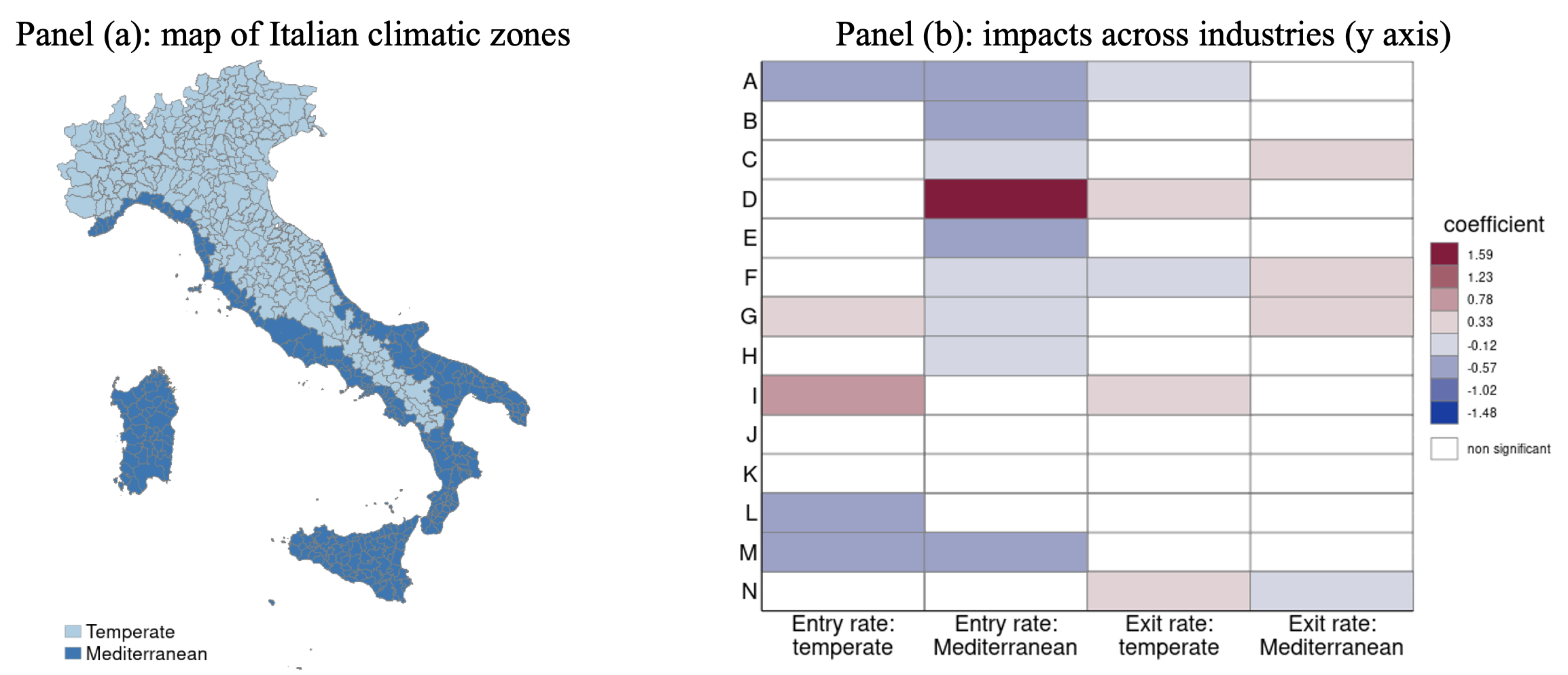

The demography analysis leverages on the Infocamere dataset, containing administrative data on more than 2 million firms per year (the universe excluding one-person companies) between 2005 and 2019. We examine the impact of temperature on the determinants of the growth rate of active firms in a local labour market: the entry of newborn firms, the exit of firms ceasing their business and the relocation of firms (within Italy or abroad). We distinguish temperature impacts across a geographic dimension linked to climatic zones – hotter Mediterranean areas, which covers most of the coastal zones, and colder temperate areas (see panel (a) of Figure 1) – as well as across industries. To proxy for heat waves, we adopt a commonly used measure of the number of days within a year with maximum temperatures above 30°C, taking temperatures from the JRC MARS Meteorological Database. As market dynamics are typically slow moving, we separately test cumulated temperature effects over three-year time spans.

The heat map in panel (b) displays the results, with red boxes indicating a positive effect of temperature, blue boxes a negative one and white boxes a null (non-significant) one. Overall, extremely high temperatures cause, in the medium term, a fall in the entry rate and, to a lesser extent, an increase in the exit rate of firms from local labour markets. Most of the action takes place in the Mediterranean zone, where impacts go beyond those on agriculture (whose effects are widespread across the country). The only sector that benefits from high temperatures in the Mediterranean zone is the electricity sector, probably because high temperatures spur electricity needs for air conditioning. Relocation towards more favourable climatic areas (not shown in Figure 1) plays a minor role: temperature impacts are negligible or not significant in almost all cases. Moreover, the lack of a clear sector-level correspondence between a higher exit (or a missing entry) in Mediterranean areas and a higher entry in temperate ones suggests that other forms of climate-induced firm mobility – such as ceasing activity in one place and re-opening in another – are, in the case of Italy, at least of secondary importance.

The effects of extreme temperatures on market structure are quantitatively relevant. As the number of days with maximum temperature above 30°C permanently increases by ten in a year, the growth rate of active firms lowers by 0.13 percentage points, almost one-tenth of the average growth rate in the sample, largely due to the reduction in the entry rate. Using the forecasted local temperatures as in the central ETHZ CLM scenario, our estimates imply a cumulated reduction in the growth rate of the corporate sector in current decade by 0.22 percentage points.

Figure 1 The effect of high temperatures on entry and exit rates in Mediterranean and temperate areas

Note: Panel (a) displays local labour markets, classified into temperate and Mediterranean climate zones according to the Istat classification. Panel (b) displays the impact of an increase of 10 extreme temperature days over a 9-year period; red boxes: positive impact; blue boxes: negative impact; white boxes: no impact. The rows of the matrix indicate the sector according to the Nace Rev. 2 classification: A. Agriculture, Forestry and Fishing; B. Mining and Quarrying; C. Manufacturing; D. Electricity, Gas, Steam and Air Conditioning Supply; E. Water Supply, Sewerage, Waste Management and Remediation Activities; F. Construction; G. Wholesale and Retail Trade, Repair of Motor Vehicles and Motorcycles; H. Transportation and Storage; I. Accommodation and Food Service Activities; J. Information and Communication; K. Financial and Insurance Activities; L. Real Estate Activities; M. Professional, Scientific and Technical Activities; N. Administrative and Support Service Activities.

Firm-level effects

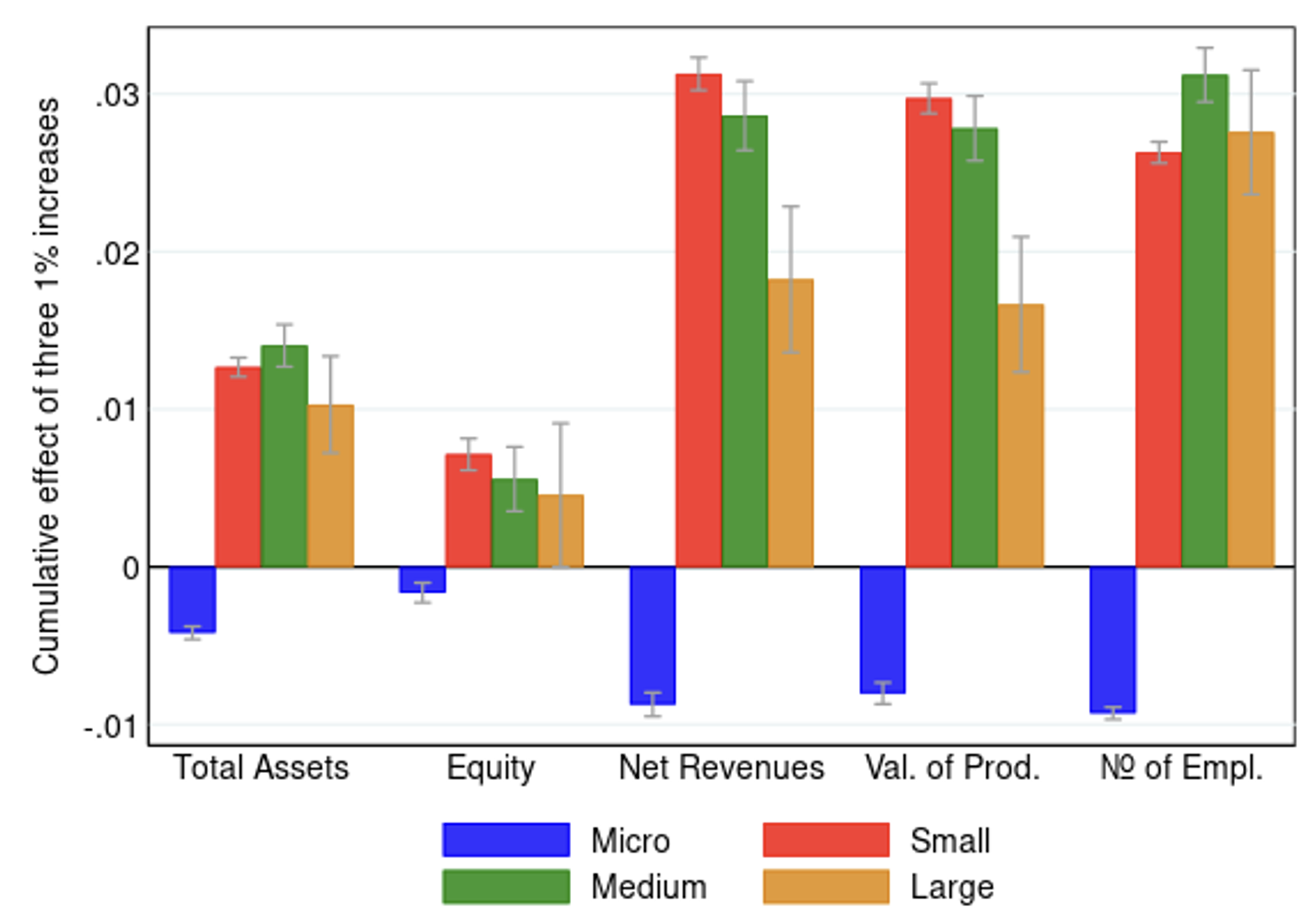

To investigate the impact of temperature on firm outcomes, we rely on almost 10 million firm-year balance sheet observations from the Cerved dataset. We divide firms into four size classes according to the Eurostat definition and explore the effects of temperatures on total assets, firm’s equity, net revenues, the value of production, and the number of employees. The results, shown in Figure 2, are quite striking. Over the medium term, firms in three out of four size classes show positive effects of temperatures, suggesting that sufficiently large firms have the ability to adapt to climate change and improve their profitability. By contrast, micro firms shrink in size – in terms of net revenues, value of production, and number of employees – confirming their inability to adapt by investing in green technology (Accetturo et al. 2022). Clearly, the sample under investigation only refers to the firms that remained active on the market over the whole observation period. Nonetheless, the analysis highlights a clear dichotomy in the resilience to climate change, which appears to be particularly detrimental for very small firms.

Figure 2 Firm-level effects across classes of firm size

Overall, our findings suggest that global warming will weigh on the corporate sector not only in terms of size but also composition. Higher temperatures could amplify the already existing different growth path between small and large firms, stimulating a re-composition within the business sector in terms of value-added creation. This may not be inconsequential for aggregate productivity growth.