Why disaster risk financing must evolve to meet the climate crisis

Climate-related disasters are increasing in frequency and severity, yet global adaptation and resilience (A&R) finance remains fragmented, reactive, and far below estimated needs. In a world increasingly shaped by climate extremes, the way we finance disaster risk is no longer fit for purpose.

The financial risks extend far beyond immediate disaster costs. Major institutional investors collectively hold approximately $5.1 trillion in fossil fuel company stocks and bonds, with U.S.-based investors alone responsible for $3.1 trillion of this total. Climate change represents a systemic, non-diversifiable risk to financial assets.Unmitigated climate change could cause losses equivalent to 1.8% of global financial assets ($2.5 trillion) by 2100, with extreme scenarios reaching 17% (over $20 trillion). Yet, the money to prepare for such events adaptation and resilience continues to arrive too late, too little, and too unevenly. The global system for disaster risk financing is highly vulnerable and unless we overhaul it, we will continue to fail the communities most vulnerable to climate shocks.

The cost of waiting for disaster

The data tells a troubling story. Climate finance tends to spike only after disasters occur. This reactive pattern is not just a policy failure it’s a moral one. It means we are choosing to rebuild what was lost rather than investing in what could have been protected.

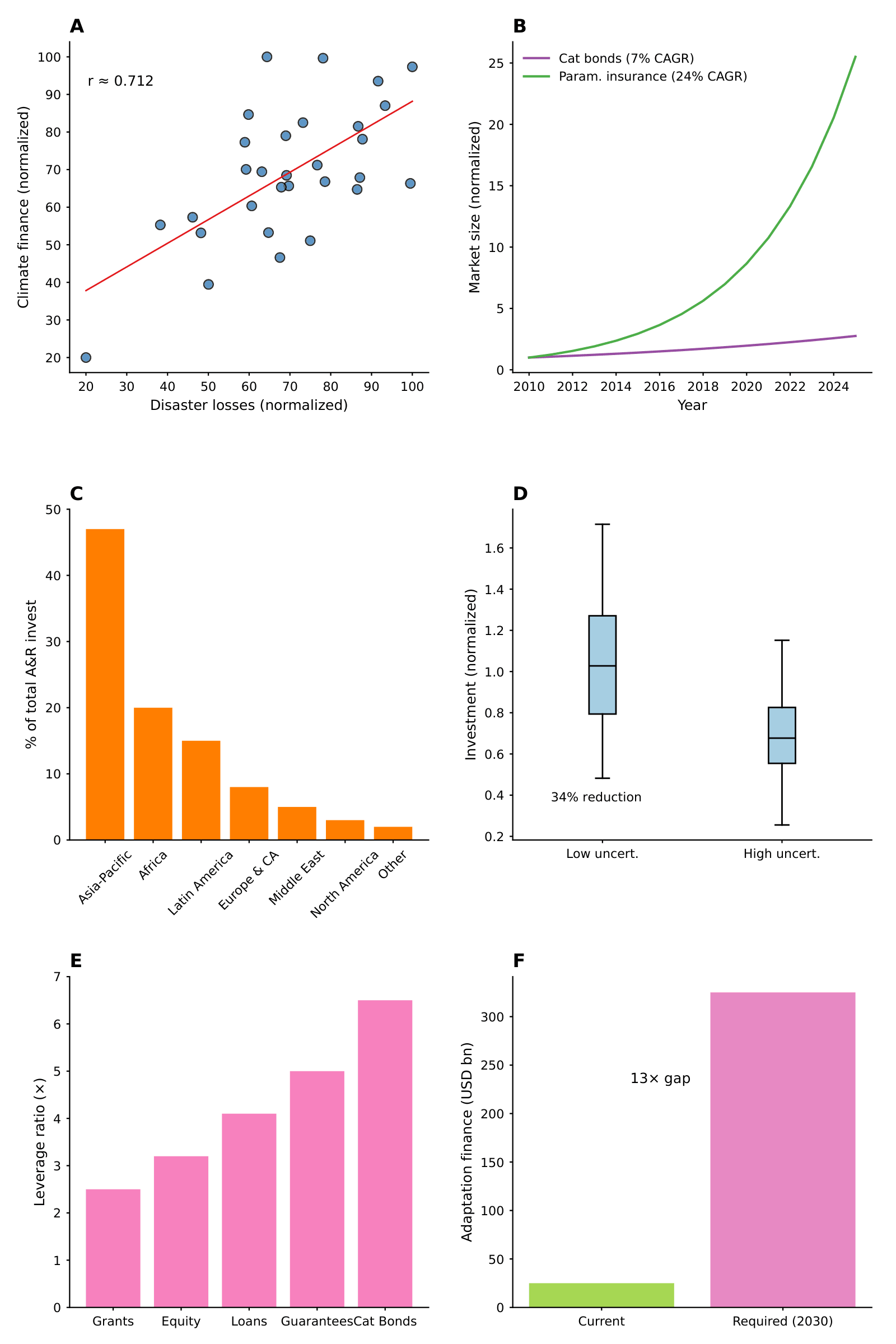

Figure below shows a strong correlation between disaster losses and subsequent finance flows, confirming that we are still stuck in a cycle of response rather than prevention. This isn’t merely a technical issue, it’s deeply rooted in politics and ethics. The communities that contribute least to climate change are often the ones left waiting for help after disaster strikes. And when that help comes, it’s often too late to prevent the worst outcomes.

Figure 1. Statistical relationships in climate resilience finance. (A) Correlation between annual disaster losses and climate finance flows (normalized), illustrating a reactive financing pattern (Pearson r=0.71). (B) Time-series growth of risk-transfer instruments (2010–2025), showing rapid expansion of parametric insurance markets (24% CAGR) relative to catastrophe bonds (7% CAGR). (C) Regional distribution of adaptation and resilience (A&R) investment, with Asia–Pacific accounting for approximately 47% of global flows. (D) Boxplot comparison of investment levels under low versus high climate policy uncertainty, indicating an approximate 30% reduction in investment during high-uncertainty periods . (E) Blended-finance leverage ratios by instrument type, highlighting higher private capital mobilization for guarantees and catastrophe bonds (up to 6.5X). (F) Global adaptation finance gap, contrasting current annual flows (US$25 billion) with estimated 2030 needs (US$325 billion), implying a 12–14X scale-up requirement. (Sources: EMDAT; Climate Policy Initiative; OECD-DAC; Green Climate Fund; Artemis; CCRIF/PCRIC/ARC; UNFCCC; IPCC).

The tools we need already exist

We don’t need to invent new technologies to fix this. We need to use the tools we already have and scale them. Parametric insurance, for example, offers rapid payouts based on pre-agreed triggers like wind speed or rainfall. It’s already working in places like the Caribbean and the Pacific, where regional risk pools such as CCRIF and PCRIC have helped countries respond quickly to hurricanes and droughts.

Catastrophe bonds are another powerful tool. They allow governments to transfer disaster risk to capital markets, providing a financial buffer when extreme events occur. The market for these bonds is growing, but it’s still far too small to meet global needs.

Blended finance combining public and private capital can unlock billions for resilience projects. But it requires leadership, coordination, and a willingness to take calculated risks.

What’s stopping us?

The main challenge isn’t about technology, it’s about having the political determination to act. When governments send unclear or inconsistent messages about their climate goals, it creates hesitation among investors. Studies show that this kind of uncertainty can cut private investment in climate adaptation by nearly one-third.

At the same time, large institutional investors who control trillions of dollars are still putting very little into climate solutions. Many sovereign wealth and pension funds invest less than 1% of their portfolios in green assets , even though the financial risks from climate change are growing..

The insurance industry, which should help manage these risks, is also facing growing pressure. As climate-related claims increase and underwriting standards weaken, the sector itself could become a source of financial instability .

A call for systemic change

We need to stop treating innovative disaster risk finance as a niche or experimental field. Countries like Mexico, Indonesia, Kenya, and the Philippines have shown that it can and must become core infrastructure embedded in national budgets, development finance, and commercial banking. Mexico’s FONDEN, for example, institutionalised disaster finance through annual budget allocations and pioneered the world’s first sovereign catastrophe bond. Indonesia’s Pooling Fund for Disasters, backed by a $500 million World Bank loan, is now a central mechanism for channelling pre-arranged finance to line ministries and local governments. In Kenya, a national disaster risk finance strategy and a $200 million Catastrophe Deferred Drawdown Option (Cat-DDO) have enabled rapid disbursement of funds after floods and the COVID-19 crisis.

Governments must lead by developing national disaster risk finance strategies that integrate pre-arranged finance, insurance, and risk reduction. Financial institutions must build the capacity to assess climate risks and offer specialised products. Investors must align portfolios with climate goals not just for ethical reasons, but to protect long-term value.

The global community must recognsze that disaster risk financing is about fairness, dignity, and the right to a future that isn’t derailed by every storm, drought, or earthquake. The next decade will determine whether we continue to finance disasters or whether we finally invest in preventing them.

Dr. Fakhruddin is a globally recognized, award-winning expert in the field of climate resilience and disaster risk reduction. He has over 24 years of experience advising governments and organizations around the world on disaster risk reduction and climate change adaptation. As a hydrometeorologist, his specialty is in climate risk assessment, early warning systems, community resilience, and water security. Dr. Fakhruddin is currently working as Climate Investment Principal and leading the Water Sector at the Green Climate Fund. He oversees climate investments in vulnerable countries around the world to support water security and early warning project origination. He serves on international expert committees, Chair, Board Member and Professor such as the International Science Council, CODATA, Earth GEO, WMO, and lends his expertise to advance national resilience agendas for governments in LDCs and SIDS.