Global Assessment Report on Disaster Risk Reduction 2015

Making development sustainable: The future of disaster risk management |

Global Assessment Report on Disaster Risk Reduction 2015

Making development sustainable: The future of disaster risk management |

|

|

150

Part II - Chapter 7

As a consequence, risk assessments, particularly in the private sector, have tended to focus more on hazards, exposure and physical vulnerability than social and economic vulnerability and resilience, on extreme intensive risks rather than recurrent extensive risks, and on applications to protect development against external threats rather than applications to transform development. For example, these assessments are meant to identify optimum levels of protection for strategic and critical infrastructure which is essential to a country’s economy, to identify options for risk transfer and financial protection, or to inform preparedness and early warning for intensive disasters (

GFDRR, 2014a GFDRR, 2014a GFDRR (Global Facility for Disaster Reduction and Recovery). 2014a,Understanding Risk: The Evolution of Disaster Risk Assessment since 2005, Background Paper prepared for the 2015 Global Assessment Report on Disaster Risk Reduction. Geneva, Switzerland: UNISDR.. GFDRR (Global Facility for Disaster Reduction and Recovery). 2014a,Understanding Risk: The Evolution of Disaster Risk Assessment since 2005, Background Paper prepared for the 2015 Global Assessment Report on Disaster Risk Reduction. Geneva, Switzerland: UNISDR.. Click here to view this GAR paper. As noted in Chapter 4 of this report, far less attention has been devoted to assessing extensive risks. Despite the magnitude of associated losses and impacts, these risks remain unaccounted for and largely invisible because the disasters rarely challenge strategic economic and political interests (Box 7.11).

Therefore, while improved interoperability, open data, sustainability and capacities may make risk information more usable and actionable, a different approach to the production of risk information is required.

Risk always implies both opportunities and costs for different stakeholders. A factory built in a hazard-exposed location but in an area with low labour costs and good access to markets may represent an opportunity for business owners and investors. However, damage from a disaster will not only affect the business, but also the workers, who may lose their employment temporarily or permanently, as well as the local economy and the government, which may lose tax receipts, among others. Risk information should clarify who takes the risks, who benefits, who pays and thus who owns the risks. It should also clarify the benefits and costs of investing in disaster risk management. In other words, in order for risk information to become risk knowledge, the basic parameters of accountability have to be clarified in a way that

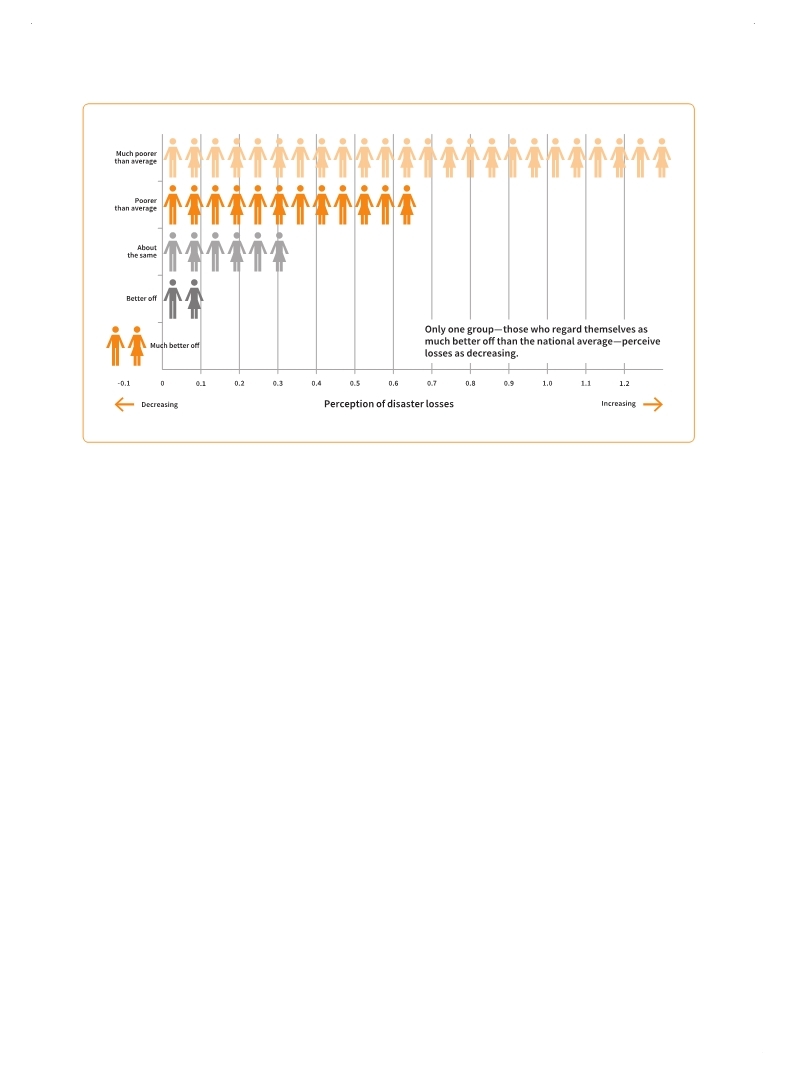

(Source: GNDR, 2013

GNDR (Global Network for Disaster Reduction). 2013,Views from the Frontline: Beyond 2015, Findings from VFL 2013 and recommendations for a post-2015 disaster risk reduction framework to strengthen the resilience of communities to all hazards.. . Figure 7.6 Perceived losses according to self-reported income level

|

Page 1Page 10Page 20Page 30Page 40Page 50Page 60Page 70Page 80Page 90Page 100Page 110Page 120Page 130Page 140Page 141Page 142Page 143Page 144Page 145Page 146Page 147Page 148Page 149Page 150Page 151->Page 152Page 153Page 154Page 155Page 156Page 157Page 158Page 159Page 160Page 161Page 162Page 163Page 164Page 170Page 180Page 190Page 200Page 210Page 220Page 230Page 240Page 250Page 260Page 270Page 280Page 290Page 300Page 310

|

|

|

|