Sovereign risk

Sovereign risk is the financial damage a government faces after a disaster.

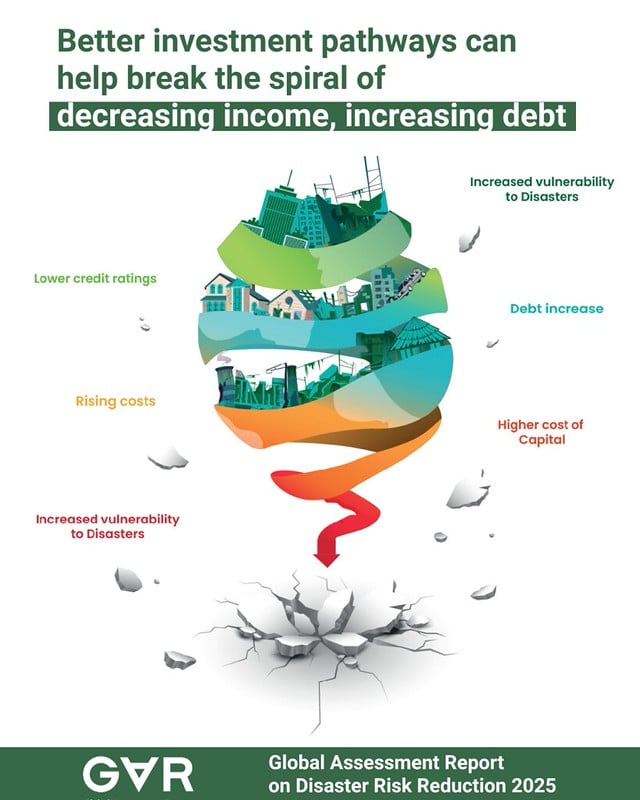

Sovereign risk refers to the financial exposure a government faces in the event of a disaster. When disaster-related costs are not integrated into national budgets, governments may struggle to meet debt obligations following a crisis. This can lead to credit rating downgrades, increasing borrowing costs through higher interest rates.

As access to affordable financing becomes constrained, the overall cost of disasters rises, potentially triggering a “debt spiral” that weakens fiscal stability and the health of public finances. Sovereign risk financing strategies aim to strengthen governments’ capacity to respond effectively to disasters while safeguarding fiscal balance.

What is sovereign risk?

The sovereign refers to the State, representing its citizens. Sovereign risk is the risk that a government will be unable to meet its financial obligations, including repaying debt and financing essential public services.

Governments raise funds by issuing bonds, and the interest rates they pay are influenced by their credit ratings. These ratings reflect investors’ assessment of the government’s ability to repay its debt, and therefore its level of risk.

In disaster contexts, sovereign risk increases as governments face sudden financial shocks: they must support affected populations while potentially facing higher borrowing costs. If disaster risk is perceived to be high, investors may demand higher interest rates, further constraining fiscal space.

Why does sovereign risk matter?

The State holds a range of financial liabilities, including both direct and contingent obligations. Direct liabilities refer to existing commitments such as public debt, budgetary expenditures, pensions, and social security payments.

Contingent liabilities are obligations that may arise depending on specific events. These can be either explicit or implicit. Explicit contingent liabilities are legally or contractually defined, such as government guarantees to subnational authorities or public and private entities, which are triggered if agreed conditions are not met.

Implicit contingent liabilities are not legally binding but are based on moral expectations of government intervention. These may include support to the financial system, social protection schemes, or post-disaster response and recovery.

Disasters can sometimes overwhelm small island economies; the economic pressure in recovering from disasters is often disproportionate to the economic capacity of Pacific Island Countries and Territories.

ODI, 2015

If these potential costs are not accounted for and a disaster occurs, governments may face significant fiscal deficits. Sovereign risk reflects the financial obligations that arise following disasters, including the costs of response, recovery, and reconstruction.

Many developing countries, particularly smaller and less diversified economies, have limited fiscal capacity to absorb such shocks. In the event of a major disaster, governments may be forced to reallocate resources from other priorities or increase borrowing to finance response efforts.

For 61 vulnerable countries, fiscal gaps could be expected at least every ten years (an annual probability of 10%). In contrast, in another set of 54 countries across low-income, emerging and advanced economies, such fiscal gaps could be expected only every 50 years (an annual probability of 2%), most likely due to lower hazard vulnerability and exposure.

What can be done to reduce sovereign risk?

In both disaster risk reduction and climate change adaptation, there is growing reliance on insurance and other risk financing instruments to manage sovereign risk and strengthen resilience. These mechanisms help governments prepare for the financial impacts of disasters before they occur.

Disasters are increasingly recognised as contingent liabilities for governments. While these obligations are not realised in normal conditions, they become actual liabilities when disasters occur, requiring public expenditure for response, recovery, and reconstruction.

Without adequate financial planning, these sudden liabilities can place significant pressure on public finances and ultimately affect society as a whole.

Governments are responsible for the safety and well-being of their populations, making resilience fundamentally a public sector concern. However, many risk financing schemes reflect a narrower focus on protecting government finances rather than societal resilience.

In practice, these mechanisms often safeguard the State and its financial obligations, particularly through international financial arrangements. This can result in limited protection for the broader population, despite the significant impacts disasters have on households, livelihoods, and communities.

Governments seeking to strengthen their disaster response capacity typically combine multiple financial instruments and policies that complement one another. A comprehensive sovereign risk financing strategy considers not only how to access resources to cover losses, but also how to reduce potential impacts in advance through risk assessment and risk reduction measures.

Because public debt—whether external or domestic—must ultimately be serviced, disasters can place significant strain on public finances. Integrating disaster risk into financial planning provides a strong incentive for governments to invest in risk identification and reduction as part of broader fiscal management.

Innovative approaches are emerging. For example, Barbados restructured approximately USD 300 million of high-interest debt through a debt-for-climate resilience swap, freeing up resources for investments in water management and flood protection before disasters occur.

Financial protection enables governments to mobilize resources rapidly in the immediate aftermath of a disaster, while helping to buffer long-term fiscal impacts. However, a comprehensive risk management strategy must go beyond financing alone, encompassing measures to identify risks, reduce potential losses, and strengthen preparedness and emergency response systems.

Within this broader framework, sovereign risk financing strategies play a key role in enhancing governments’ capacity to respond to disasters while safeguarding fiscal stability. These strategies draw on a range of financial instruments, each with distinct cost structures and functions.

These instruments can be grouped into two categories: ex-post financing (used after a disaster) and ex-ante financing (planned in advance).

Ex-post instruments are funding sources that do not require prior planning. They are mobilized after a disaster occurs and include budget reallocation, domestic or external borrowing, tax increases, and donor assistance.

Ex-ante instruments require proactive planning before a disaster. They include reserve or calamity funds, budget contingencies, contingent credit facilities, and risk transfer mechanisms.

Within ex-ante approaches, risk transfer instruments shift financial risk to a third party. These include traditional insurance and reinsurance, parametric insurance, and alternative risk transfer (ART) tools such as catastrophe bonds (CAT bonds).

| Ex-post | Ex-ante |

| Ex-post instruments are sources that do not require advance planning. | Ex-ante risk financing instruments require pro-active advance planning. |

| Examples: Budget reallocation, domestic credit, external credit, tax increase, donor assistance. | Examples: Reserves or calamity funds, budget contingencies, contingent debt facility, risk transfer mechanisms. |

Breaking the spiral: Solutions from the GAR 2025

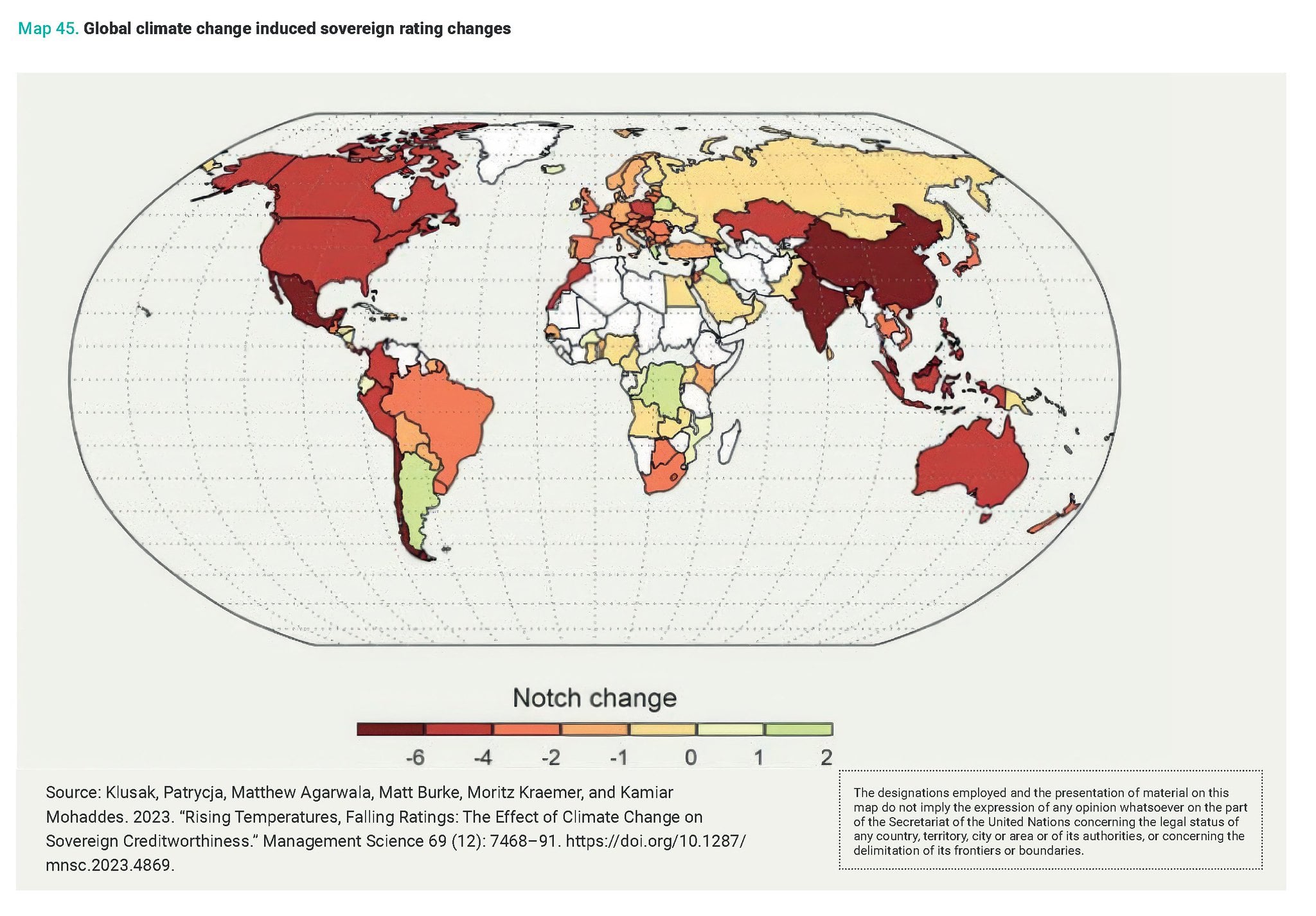

According to the GAR 2025, sovereign risk can be reduced by shifting from a “respond–recover–repeat” model to a more proactive strategy. This includes using innovative tools such as Special Drawing Rights (SDRs) to provide rapid liquidity, implementing budget tagging to track resilience and adaptation spending, and developing “adaptation-smart” credit ratings to help prevent costly debt spirals.

Strategic investments in proactive measures such as early warning systems, community preparedness, and hazard-proofing housing and infrastructure have helped Fiji maintain its credit rating despite experiencing high-intensity disasters. Incorporating resilience investments into credit rating assessments can strengthen a country’s creditworthiness. One study found that if disaster protection and resilience investments were integrated into assessments across the region, the average credit rating of the 13 SIDS analysed would increase from a moderate 6.59 to 7.49.

Governments can also strengthen awareness of their resilience investments through budget tagging. By labelling, quantifying and tracking resilience-related public expenditure in an integrated manner, governments can improve resource allocation and spending efficiency. In Kenya and Madagascar, UNDRR supported governments in establishing such systems to mainstream disaster risk reduction and climate change adaptation across sectoral budgets. Tracking expenditure over time also enables more accountable, evidence-based decision-making by providing critical insights into spending patterns and performance.

Financing instruments

An enabling regulatory and supervisory framework is essential to ensure a strong insurance sector with sufficient financial capacity to absorb—and where appropriate transfer—disaster risks. It also helps ensure that risk is accurately priced, thereby encouraging risk reduction.

An effective financial strategy for disasters relies on a combination of instruments. These should be selected based on the country’s fiscal risk profile, the cost of available tools, and the expected disbursement needs following a disaster.

A comprehensive disaster risk assessment—identifying exposures and interdependencies—is critical for designing effective strategies. Strong leadership from Ministries of Finance is also crucial for the development and implementation of integrated disaster risk financing approaches.

Related stories

Last updated: April 2026