Risk Rating 2.0: A first look at FEMA’s new flood insurance system

Risk Rating 2.0 has been called the Federal Emergency Management Agency’s (FEMA)’s most significant reform in 50 years. Roughly 77% of customers of the National Flood Insurance Program (NFIP) nationwide will see increases in their premiums, while the other ~23% will see reductions or no change. FEMA will formally introduce Risk Rating 2.0 on October 1, 2021, and most premium increases will kick in on April 1, 2022.

In brief, Risk Rating 2.0 moves the NFIP away from its heavy reliance on in-or-out flood zones, in particular in-or-out of the so-called “100-year floodplain,” and towards an individual assessment of risk for each property. FEMA’s 100-year flood area will not go away – in particular, this will still be the basis for whether a property owner with a federal mortgage must buy flood insurance – but the premiums for each property will be determined based on individual factors that include flood risk from an ensemble of three privately developed flood models.

The Data

Recently, FEMA published summaries of NFIP premium changes by state, with details down to individual zip codes. This first glimpse of Risk Rating 2.0 is a limited one; for example it shows only first-year changes (increases are capped at 18%/year) and lumps the most extreme increases or decreases into bins of “greater than $100” per month. Nonetheless, our group took the zip code-level data and “reverse engineered” that information to provide a first look at what policyholders and others interested in flood-risk management can expect from Risk Rating 2.0.

The focus of this review is California. Over the history of the NFIP, California has been a donor state, contributing hundreds of $millions more in flood insurance premiums than it has received in claims (California Water Blog 12/14/2016). Under Risk Rating 2.0, 73.2% of California NFIP policyholders will see premiums increase, and 26.8% will see decreases.

We encourage readers to explore Risk Rating 2.0 premium changes across California using our interactive map of average premium changes by zip code (Link to Interactive Map).

Premium Changes and Patterns across California

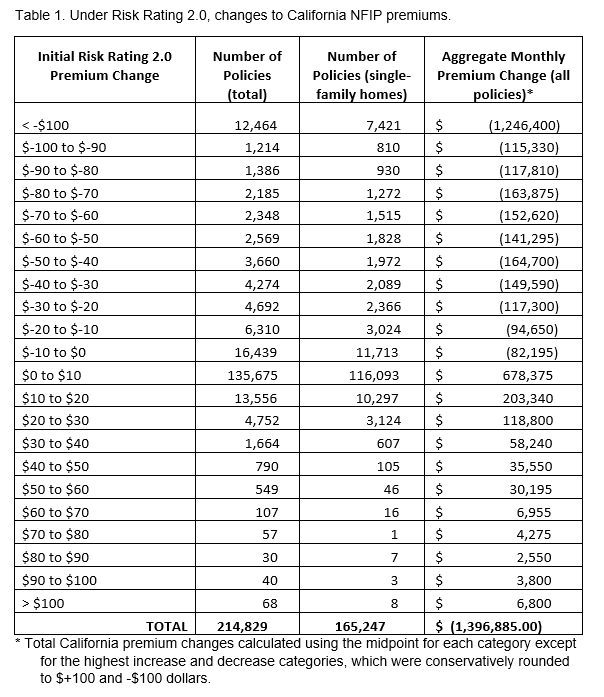

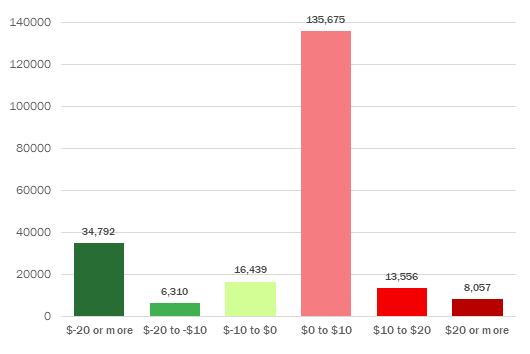

Statewide, the majority of Californians with NFIP policies can expect to see premium increases of less than $10 per month (Figure 1; Table 1). That being said, the total amount of premium dollars paid by California policyholders as a whole is actually set to decrease. The overall distribution of premium changes across California is bimodal – a large majority of policyholders will receive small rate increases, but some policyholders will receive larger discounts. Of the >20,000 policies receiving discounts of ≥$20 per month, nearly half are >$70/month. We cannot precisely calculate the total net impact of Risk Rating 2.0 on California because FEMA’s data masks the exact dollar amount of changes at the extreme tails (8 policies with increases >$100 per month and 7421 properties with decreases >$100 per month). For the purposes of this analysis, we conservatively assumed a $100 change for the extreme tails (+/- >$100/month). Using this method, the total change in premiums in the first year of Risk Rating 2.0 is an aggregate decrease of at least $1.4 million per month (= at least $16.76 million per year statewide), or ≥9.9% of total California NFIP premiums (FEMA, 2021b). About half of this estimated total discount discount will go to single-family homes (~165,000 policies), and the other half going to the remaining non-single-family and non-residential NFIP properties (~49,000) in California.

The overall downward shift in premiums is consistent with our earlier findings that NFIP seemed to be overestimating flood risk in California. The state has been hit by more than its share of disasters, but several decades of flood data were not adding up to the flood hazard suggested by NFIP premiums until now. In shifting to a more physical, individualized formula, Risk Rating 2.0 seems to be recognizing this earlier overestimate, although not correcting the formula as much as may be warranted.

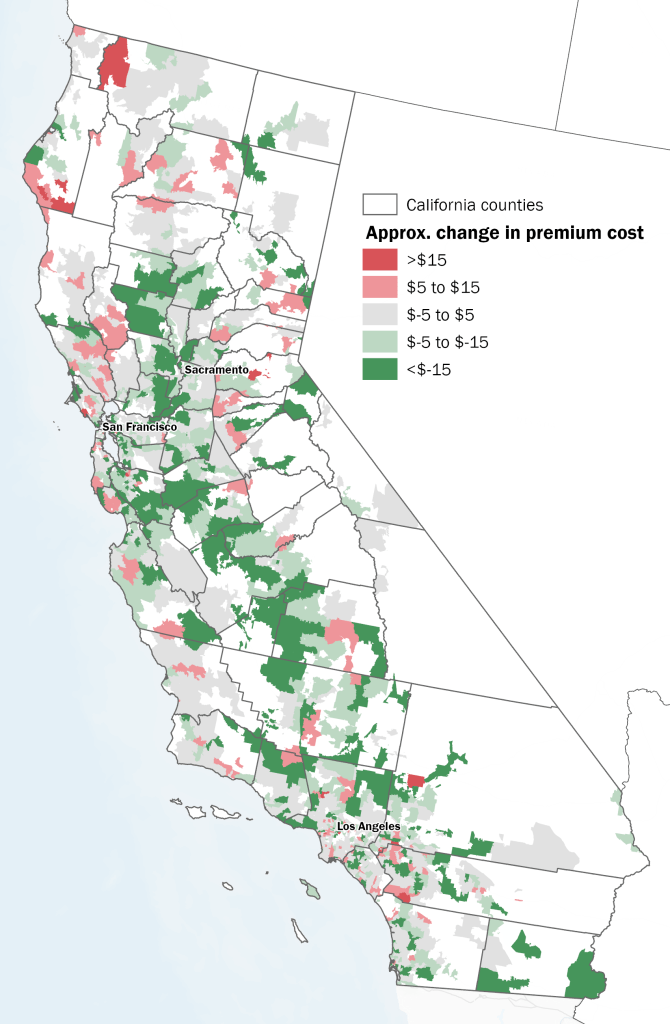

This bimodal distribution of premium changes is also interesting when mapped across California (Figure 2). Increases and decreases are scattered across the statewide zip codes, but a few regional patterns emerge. First, the California Central Valley – including the Sacramento Valley north of Sacramento and the San Joaquin Valley to the south – is characterized by average premium decreases. under Risk Rating 2.0 (greens in Fig. 2).

Stakeholders in the Central Valley have long complained that NFIP was overcharging them; for example, pressing the Government Accountability Office in 2014 to study perceived biases against agriculture baked into the NFIP. In addition, the California Central Valley has broad areas protected by levees, some of which meet the 100-year protection standard, some not.

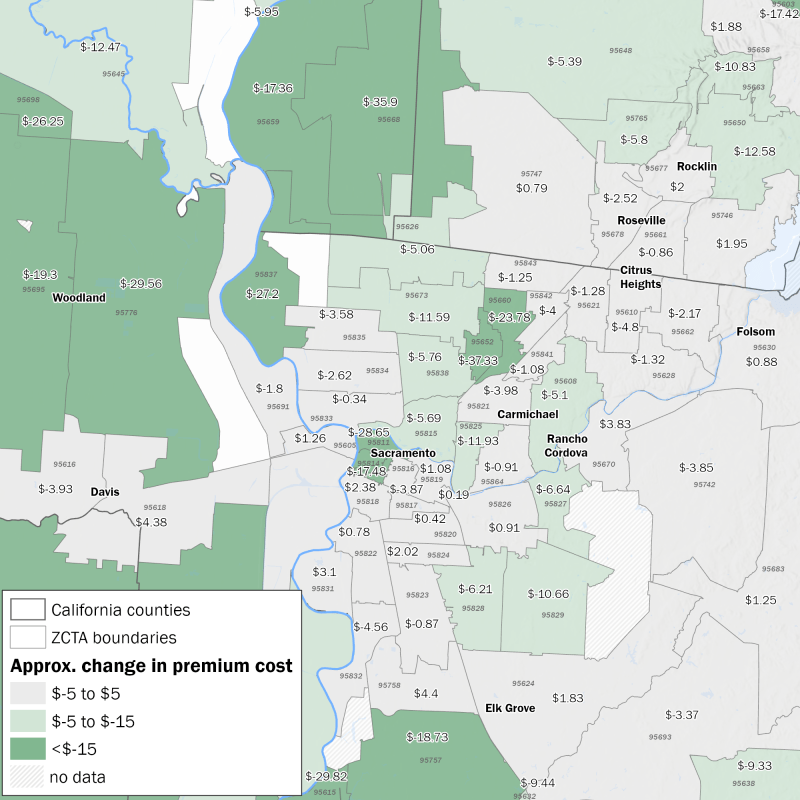

Figure 3 maps out premium changes in the Sacramento area. Four of California’s top five zip codes with the most NFIP policies are located around Sacramento. Under Risk Rating 2.0, three of those (95833, 95834, and 95835 [Natomas]), will see modest declines in premiums. Conversely, 95831 (the Pocket area) will see premium increases. All four of these are levee-protected areas along the Sacramento River. The US Army Corps of Engineers recently completed significant levee improvements around Natomas[1], and is commencing improvements to the Pocket area.[2] Until now the NFIP handled levees as all-in or all-out, a practice widely criticized from all sides. Under Risk Rating 2.0, the Corps has supplied FEMA with levee data, but estimates of levee reliability is notoriously difficult to quantify, and the new algorithm for levee protection is currently a black box that needs scrutiny.

Our own zip codes here in Davis illustrate some of the odd shifts under Risk Rating 2.0. The 95616 zip code, including western Davis and the university, will see average decreases of almost $4.00 per month, while 95618 to the east will see increases >$4.00. Both areas lie at similar elevations and are largely outside of FEMA’s mapped 100-year floodplain. The whole area is protected from flooding of the Sacramento River and other tributaries by levees and bypasses. We initially suspected that the private-sector flood models embedded in Risk Rating 2.0 are favoring levee-protected areas, making this change in Davis puzzling, but a lack of transparency in underlying data obscures the mechanisms driving such changes.

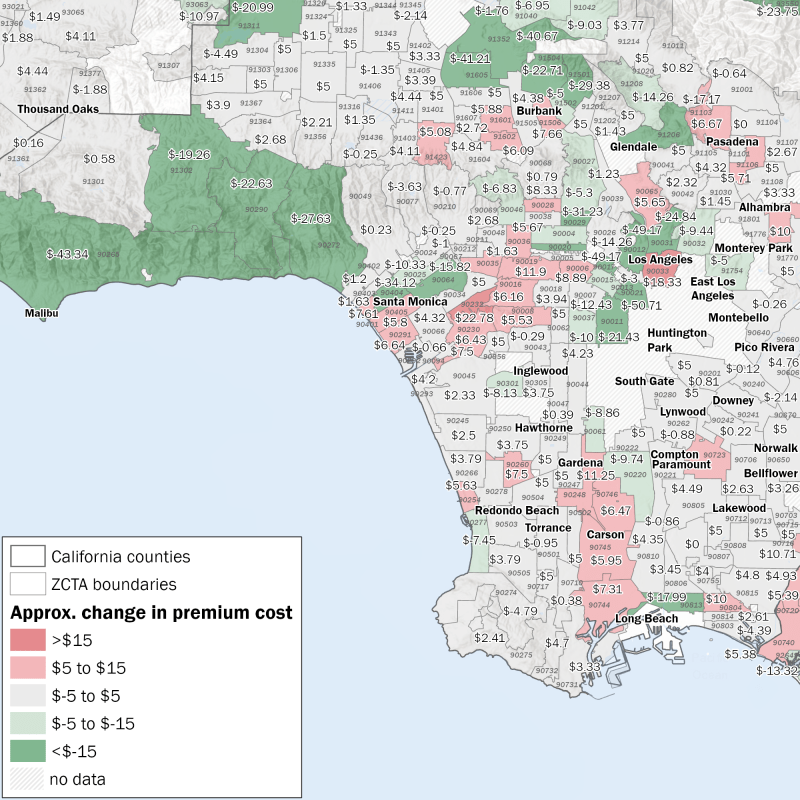

Figure 4 shows Risk Rating 2.0 premium changes in the Los Angeles area. Within this region, changes are most pronounced in the foothills and coastal areas in Malibu, the Santa Monica foothills, and the Hollywood Hills, with policyholders in zip code 90265 (Malibu) set for an average discount of >$40/month. This represents the steepest discount for any zip code in California with >1,000 current policies. Elsewhere in L.A., the densely populated San Fernando Valley and main L.A. Basin area, on average, will see modest increases in monthly premiums.

The large premium decreases in Malibu, the Santa Monica foothills, and the Hollywood Hills are surprising. FEMA is heavily marketing Risk Rating 2.0 as “Equity in Action.” Malibu’s median household income is >$150,000 per year (2019), 2.5 to 3 times higher than the $50,000-$60,000 in most San Fernando Valley zip codes.

Risk Rating 2.0 does include one important fix that promotes economic fairness. Under the current NFIP pricing system, premiums are based on the insured value of a structure and not the actual value of that building. And currently, coverage up to $60,000 is charged at a higher rate than coverage above that threshold. FEMA originally did this to encourage policyholders to insure the full value of their structure and contents (up to allowable caps). But the policy is regressive as well as counterintuitive, as high-value structures are also more likely to incur expensive damages. Under Risk Rating 2.0, premiums will be priced based on a structure’s replacement cost.

Beyond the clear fix in premium pricing above, it is unclear how much Risk Rating 2.0 lives up to its “Equity” label, either in intent or in its impact. By all accounts, Risk Rating 2.0 was designed primarily and from the start as a new pricing structure to fix NFIP’s perennial funding shortfall. As the Congressional Research Service put it, “Risk Rating 2.0 will continue the overall policy of phasing out NFIP subsidies.” Fixing the perennial hemorrhaging of NFIP may be a worthy goal, as is making insurance rates that better reflect risk, but rolling out these changes under the banner of “Equity” is disingenuous.

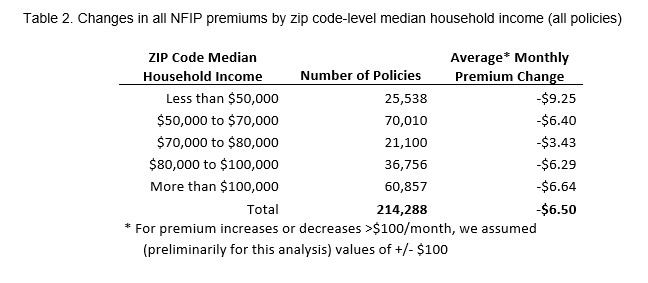

To preliminarily assess the economic equity of Risk Rating 2.0, we compared premium changes across California to median household incomes in the same zip codes (Table 2). There is no clear correlation between neighborhood income level and average premium change. Premium decreases were largest in the lowest-income category (averaging -$9.25/month for neighborhoods with incomes <$50,000). Premium decreases were smallest for middle incomes (averaging -$3.43/month for neighborhoods with incomes $70,000-$80,000). Premium changes in all other income categories, including areas with mean incomes >$100,000, were intermediate, averaging -$6.50/month.

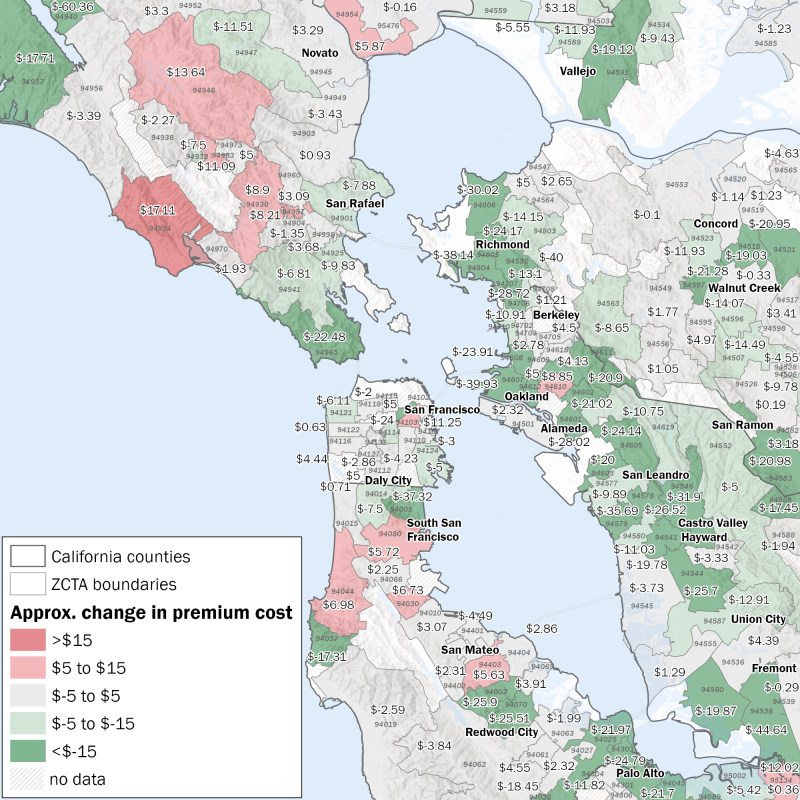

Other questions about Risk Rating 2.0 focus on the modeling and formulas used to calculate risk and premiums. Some details have been provided (e.g., the “Milliman Report,” April 2021), but a lot of Risk Rating 2.0 is a black box. Our research group is trying to obtain better, clearer data to assess questions like how coastal flooding and future climate change are reflected in the new RR2.0 premiums. In the meanwhile, Figure 5 shows zip code-level premium changes for the San Francisco Bay Area. Here, it appears that many low-lying costal areas are set to experience premium increases, while foothill areas are set for significant discounts. Coastal zip codes like 94080 (South San Francisco), 94044 (Pacifica), and 94030 (Millbrae) are will see premium increases in the $5-%7 range, while mountainous, suburban areas like 94605 (Oakland Hills) and 94583 (San Ramon) are set for premium decreases >$20 per month. However patterns in the San Francisco Bay Area appear to run counter to the Los Angeles area: average premiums in low-lying coastal areas of San Francisco going down, versus scattered decreases in Los Angeles. Deconvolving the overlapping hydraulic, climatic, engineering, and actuarial changes embedded in Risk Rating 2.0 will require much more openness and data sharing on the part of FEMA and its partner modeling contractors.

Conclusions

Risk Rating 2.0 is FEMA’s effort to bring about significant reform to the NFIP, with an eye toward incorporating more accurate flood risk information and, purportedly, more equitable premiums proportionate with that risk. Limited pricing data released by FEMA suggest that most California policyholder will see modest increases, whereas a smaller number of policyholders will see larger discounts which bring down the total NFIP bill to California by at least 10%. Mapping these data highlights how these increases and decreases vary widely across the state, and FEMA continues to mask the “extreme tails” of the distribution (changes >$100/month, i.e., >$1200 per year) as well as changes beyond the first year of Risk Rating 2.0. Also importantly, the premium decreases across California are smaller than the documented imbalance between what the state has paid into the NFIP as premiums and what its policyholders have received as payouts over the history of the program (California Water Blog, 12/14/2016).

Answering questions about Risk Rating 2.0, like the one above, requires independent scrutiny of the modeling and assessing assumptions on which the new insurance premiums are based. High on that list of important questions is how data provided to FEMA by the Army Corps of Engineers characterize flood risk behind different levees. “Levee fragility” and “residual risk” behind levees are notoriously difficult to assess and quantify, and slightly different assumptions can mean huge differences in the insurance bills that policyholders are soon to receive.

Starting on October 1 of this year, flood insurance customers eligible for renewal can lock in the new premiums under Risk Rating 2.0. Policyholders should check with their insurance agent whether their bills are slated to go up or down, and if down, by all means they should reset as soon as possible. On April 1, 2022, the new changes will apply to all new and renewing policies.

While the apparent net decrease in California’s flood-insurance premiums is a welcome change, important questions remain about how private-sector flood models and assumptions about local risk (e.g., levee protection) are weighed in Risk Rating 2.0. We call for more transparency and dialog with FEMA, including the sharing of additional information and data at a fine-grained spatial resolution.