Global Assessment Report on Disaster Risk Reduction 2013

From Shared Risk to Shared Value: the Business Case for Disaster Risk Reduction |

Global Assessment Report on Disaster Risk Reduction 2013

From Shared Risk to Shared Value: the Business Case for Disaster Risk Reduction |

|

|

|

153

nities, particularly in those countries, is undeniable (FAO and UNIDO, 2009; ILO, 2012

ILO (International Labor Office or Organization). 2012.,Global Employment Trends 2012., Geneva,Switzerland: ILO. . World Bank. 2008b.,World Development Report 2008: Agriculture for Development., Washington DC: World Bank,. . IMF (International Monetary Fund). 2012.,Regional Economic Outlook. Sub-Saharan Africa: Maintaining Growth in an Uncertain World., World Economic and Financial Surveys. October 2012., Washington D.C: IMF.,. . Thus, disasters in the agricultural sector are not only disasters for agribusinesses, large or small, but they also affect rural societies, urban households, national and global commodity markets and food security. And yet, only 14 percent of the 94 countries reporting on progress in implementing the HFA (see Chapter 14 and Annex 3) undertake disaster risk assessments prior to investment in agriculture. The risks associated with agribusiness investments become costs shared with all who purchase and consume food and agricultural commodities throughout the world. Therefore, decisions taken by agribusiness in factoring disaster

risk considerations into its investments will play a crucial role in global food security.

10.1

The agricultural

value chain

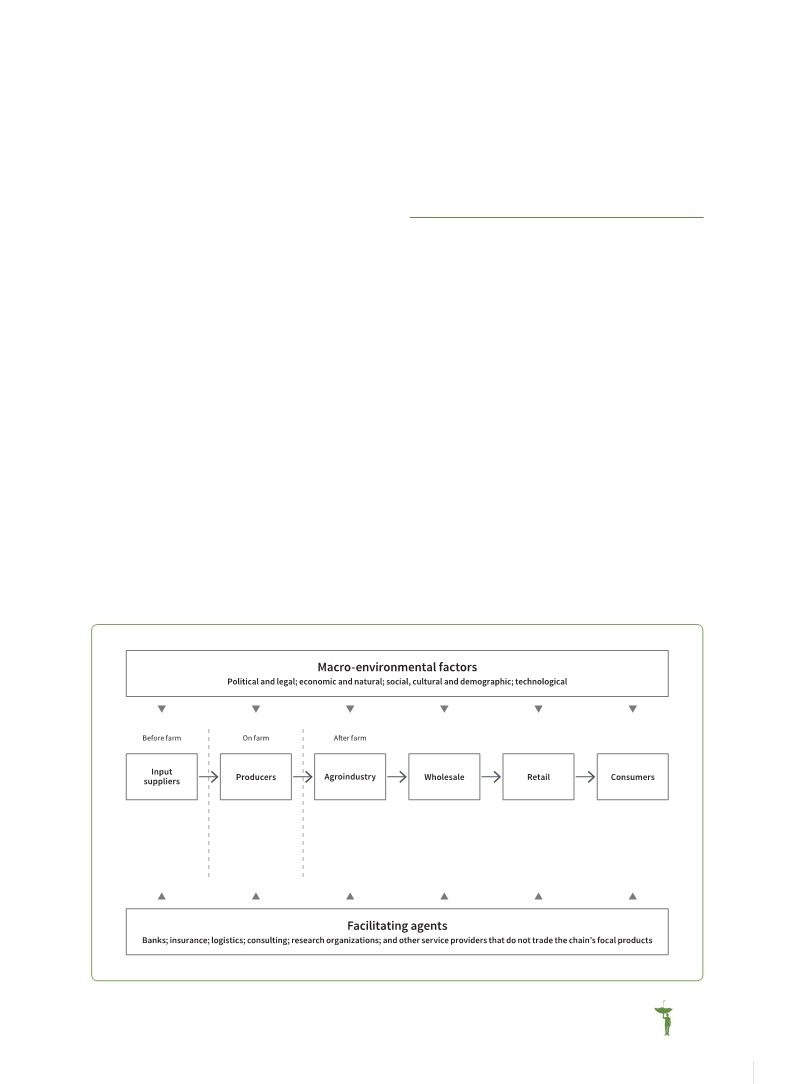

The complexity of value chains in the agribusiness sectormeansthatinterruptionsatcriticalpointsor nodes can ripple through the entire supply chain.

The agribusiness sector is organised around a complex value chain—input suppliers, producers, intermediaries, processors, marketers and consumers, mediated by a range of facilitating agents and macroenvironmental factors (Figure 10.2).

Along this value chain, size and form of businesses vary immensely; from large fertiliser companies to individual farm households that sell surplus production to local buyers at the farm gate; from local grain mill cooperatives to mediumsized processing plants; from small urban traders to multinational food chains.

(Source:

Fava Neves and Alves Pinto, 2012 Fava Neves and Alves Pinto, 2012 Fava Neves, M. and Alves Pinto M. 2012.,Analysis of the relationship between public regulation and investment decisions for disaster risk reduction in the agribusiness sector., Background Paper prepared for the 2013 Global Assessment Report on Disaster Risk Reduction., Geneva,Switzerland: UNISDR.. Fava Neves, M. and Alves Pinto M. 2012.,Analysis of the relationship between public regulation and investment decisions for disaster risk reduction in the agribusiness sector., Background Paper prepared for the 2013 Global Assessment Report on Disaster Risk Reduction., Geneva,Switzerland: UNISDR.. Click here to view this GAR paper. Figure 10.2 Framework of a typical agribusiness production chain

|

|